Returns not costing much in risk for top growth options

Many of the top performing superannuation funds’ growth options from the last three years have delivered on returns without compromising much on risk, data from FE Analytics has revealed.

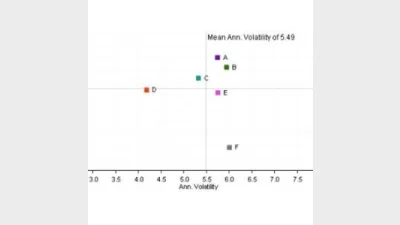

Looking at the high growth options of the five funds to perform strongest in the recently calculated Super Fund Crown Ratings, they achieved returns in excess of 10 per cent while also largely only experiencing volatility of five to six per cent.

AustralianSuper’s high growth option, for example, delivered members with returns of 11.12 per cent for the three years to this February’s end, with volatility of 5.94 per cent and a Sharpe ratio of 1.28. Over 10 years, its risk increased slightly, with volatility hitting 6.37 per cent, but its Sharpe stayed low at 1.03 and its returns were over 10 per cent.

QSuper’s aggressive option showed similar results. Its three-year returns to 28 February were 10.22 per cent with relatively low volatility of 4.18 per cent and a Sharpe ratio of 1.61. As with AustralianSuper, its risk exposure jumped slightly over 10 years, recording returns of 10.96 per cent, volatility of 6.3 per cent and a Sharpe of 1.18 for the decade to February’s end.

Proving that they do well in more than just performance, other funds to do well under the Super Fund Crown Ratings also saw parallels to the above in their returns and risk exposure.

NGS Super’s high growth option delivered returns of 10.69 per cent with volatility of 5.32 per cent and a Sharpe ratio of 1.35 for the three years to last month’s end. Statewide Super’s high growth option showed 11.51 per cent, 5.74 per cent and 1.4 for returns, volatility and Sharpe respectively over that period, and AustSafe’s super growth option delivered 9.52 per cent, 6.05 per cent and 0.81 for those three metrics for the three years to January’s end.

These returns outperformed those of the sector average, delivering higher returns with lower volatility and a higher Sharpe, meaning the level of return above that of a risk-free investment was higher. The graph below charts this comparison

The Mixed Asset – Aggressive sector, which measures high growth superannuation options, experienced returns of 7.93 per cent, volatility of 6 per cent and a Sharpe ratio of 0.74 for the three years to this February’s end. Its ten-year performance similarly underperformed the above funds’ options, with returns of 8.16 per cent for the period while recording volatility of 6.4 per cent and a Sharpe of 0.73.

Recommended for you

Australia’s largest super funds have deepened private markets exposure, scaled internal investment capability, and balanced liquidity as competition and consolidation intensify.

The ATO has revealed nearly $19 billion in lost and unclaimed super, urging over 7 million Australians to reclaim their savings.

The industry super fund has launched a new digital experience designed to make retirement preparation simpler and more personalised for its members.

A hold in the cash rate during the upcoming November monetary policy meeting appears to now be a certainty off the back of skyrocketing inflation during the September quarter.

TOP PERFORMING FUNDS

ACS FIXED INT - AUSTRALIA/GLOBAL BOND

Fund name

3y(%)pa

1

DomaCom DFS Mortgage

215.17 3 y p.a(%)

2

Loftus Peak Global Disruption Fund Hedged

118.15 3 y p.a(%)

3

Global X 21Shares Bitcoin ETF

75.00 3 y p.a(%)

4

UBS Solactive Global Pure Gold Miners UCITS ETF Dis USD

61.11 3 y p.a(%)

5

Global X Ultra Long Nasdaq 100 Complex ETF

60.93 3 y p.a(%)